ARES Urbanexus Update #179

The American Real Estate Society (ARES) distributes this periodic newsletter, which features real estate-related news and information curated by H. Pike Oliver, FAICP.

Industrial

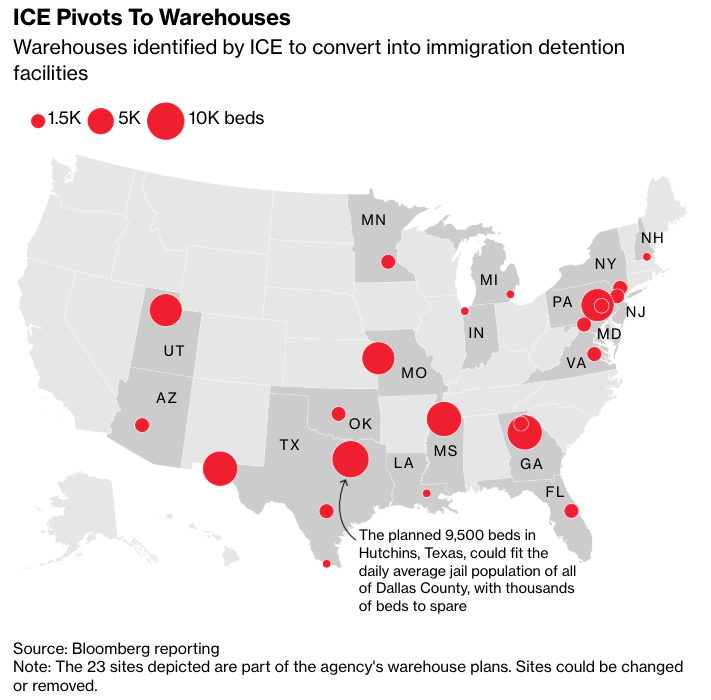

ICE is acquiring and converting warehouses into detention centers

U.S. Immigration & Customs Enforcement (ICE) plans to spend $38.3 billion to acquire large industrial warehouses and convert them into high‑capacity detention and processing facilities. The cost for just two of these properties was $172 million.

These facilities—often hundreds of thousands of square feet—are rapidly retrofitted for mass intake and short‑term holding, a process dominated by private contractors who can deliver specialized build‑outs at scale. One of them, in El Paso, Texas, could be among the largest jails of any kind in the country.

Federal agencies are exempt from local zoning and land‑use regulations. This allows ICE to convert industrial properties into detention centers without municipal approvals, enabling unusually fast deal execution and making older or underutilized warehouses far more liquid than in typical private‑market transactions. This bypassing of local entitlement processes means landlords can secure long‑term, government‑backed leases with minimal friction.

Civil‑rights groups warn about the implications of industrial‑scale detention, but for investors, the trend signals a countercyclical, policy‑driven demand driver—especially in logistics‑heavy, lower‑rent industrial submarkets where large footprints, freeway access, and political insulation align with ICE’s operational approach.

Learn more here, here and here.

Housing

An enduring U.S. bias toward single‑family housing

A reflection on Daniel Patrick Moynihan’s The Negro Family (1965) by your curator argues that, while the report did not create the single‑family bias in U.S. housing policy, it reinforced it at a pivotal moment. By framing the nuclear family as the normative household structure and overlooking the resilience of extended kinship networks, the report helped validate federal programs already privileging single‑family suburban homeownership.

Federal Housing Administration loan underwriting, GI Bill and VA loan practices, the mortgage interest deduction, and Government Sponsored Enterprise financing standards all continued to channel capital toward single‑family homes while sidelining multigenerational and flexible housing forms. Combined with exclusionary zoning, these policies shaped a built environment misaligned with the diverse household structures common among Black, immigrant, and working‑class communities. Contemporary zoning reforms in California, Oregon, and Minneapolis—legalizing duplexes, triplexes, and ADUs—represent a gradual shift away from this legacy toward more inclusive housing options.

Learn more here.

Daniel Patrick Moynihan, The Negro Family: The Case for National Action (Washington, D.C.: U.S. Department of Labor, 1965), https://www.dol.gov/sites/dolgov/files/OASP/legacy/files/moynihan.pdf

The unhoused population in the USA

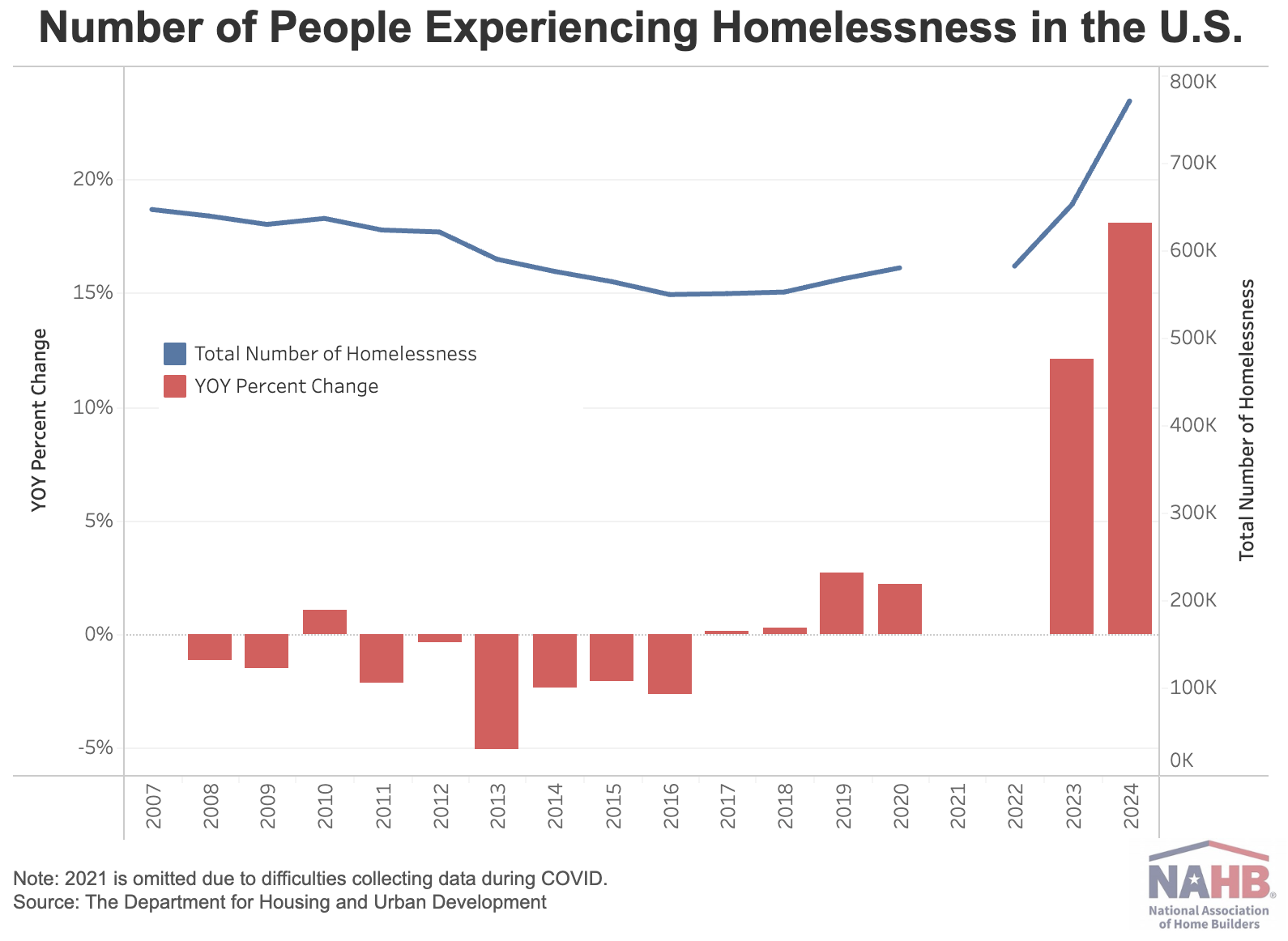

A December 2025 Eye on Housing analysis reports that the U.S. homeless population reached a record 771,500 people in the January 2024 HUD Point-in-Time count—an 18% year-over-year increase and the largest single-year increase ever recorded. Nearly all demographic groups saw rises: individuals increased by 10%, families with children surged 39%, unaccompanied youth grew 10%, and chronic homelessness went up 7%. Veterans were the only group showing a decline, continuing a long-term downward trend.

California and New York accounted for the largest numbers of people experiencing homelessness, while Hawaii and New York had the highest rates relative to population. Only seven states and Puerto Rico posted declines. Sheltered homelessness rose sharply (up 25%), reflecting the January timing of the count, and now represents 64% of those counted.

The article links the surge to worsening housing affordability—more than half of renters are cost‑burdened and most households cannot afford a median‑priced home—driven by high mortgage rates, strong demand, and a decade of underbuilding. Long‑term mitigation, it argues, requires expanding overall housing supply, while near‑term responses depend on increasing the supply of affordable units and strengthening tools such as the Low‑Income Housing Tax Credit.

The full article is available here.

Performance of modular and prefabricated construction in the USA

A recent analysis by Devan Reddy reviews why the past decade’s wave of venture‑backed modular and prefabricated housing firms—such as Katerra, Veev, Entekra, Blu Homes, Factory_OS, and Revolution Precrafted—delivered poor returns despite significant investment. Four structural factors undermined these ventures: factory economics, barriers to builder adoption, regional market fragmentation, and misaligned capital expectations.

Modular factories need high and steady utilization to be cost-effective, but construction demand is cyclical, interest-rate-sensitive, and project-based. Many companies worsened this mismatch by overbuilding factories, automating too early, and assuming that scaling up would increase demand. Adoption by builders also lagged. Mid-sized builders faced operational risks from changes in sequencing and inspections, while large builders had little reason to change their established processes. Many modular companies pushed for system-wide changes instead of fitting into existing workflows.

Regional variation in codes, climate, zoning, and trade ecosystems further constrained scalability. Modular production depends on standardization and regional factory radii, but U.S. housing markets are highly localized and tied to irregular land pipelines, making manufacturing‑style throughput difficult. Scaling required additional factories, each carrying its own demand risk.

Finally, venture capital expectations for rapid growth and high margins clashed with the slow‑cycle, thin‑margin realities of construction manufacturing. Large capital infusions often accelerated failure by pushing premature expansion, as seen with Katerra’s rapid overreach. Rising interest rates in 2023 exposed firms whose operations were not self‑sustaining.

Reddy concludes that these failures reflect misaligned business models rather than the impossibility of industrialized construction. More viable approaches would emphasize smaller, regionally matched factories, component‑level integration, incremental process improvement before automation, demand‑driven production, and patient capital aligned with long‑cycle industrial assets.

Learn more here.

Reducing affordable housing costs in the Bay Area

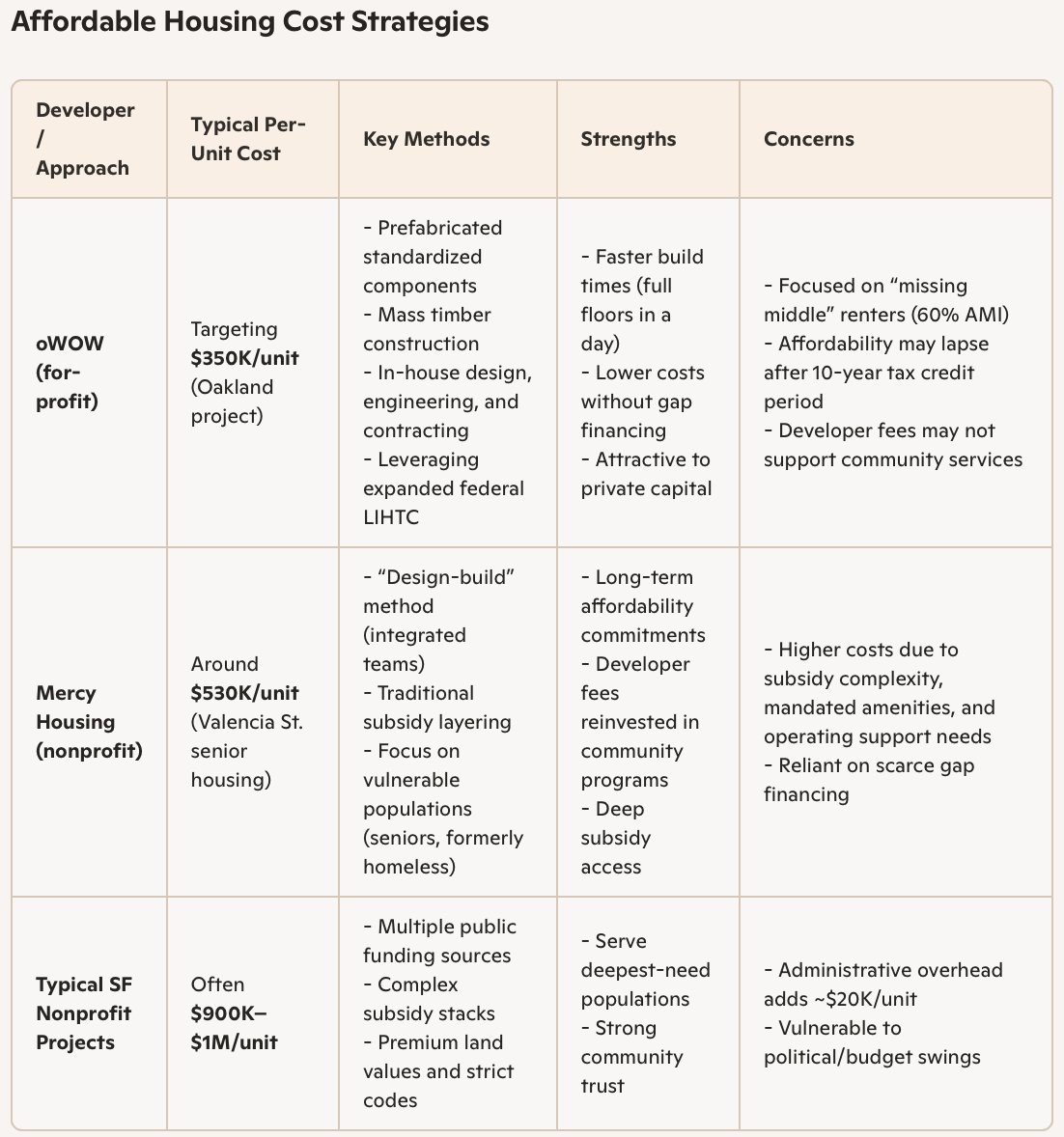

In the San Francisco Bay Area, building a single affordable housing unit can cost close to $1 million, rivaling luxury condo prices. Developer Danny Haber and his company, oWOW, claim they can deliver units for about $350,000 each by streamlining construction and leveraging expanded federal Low-Income Housing Tax Credits (LIHTC). Their approach includes prefabricated components, mass timber, and in-house design and construction teams to cut costs and avoid delays.

oWOW is breaking ground on 284 affordable apartments in downtown Oakland and has additional projects in San Francisco. They represent a wave of market-rate developers entering the affordable housing sector as traditional financing for luxury projects stalls. The LIHTC expansion, a policy shift from the Trump era, has created new opportunities, with California approving 25,781 units in 2025, a sharp increase from the prior year.

Nonprofit developers like Mercy Housing and Bridge Housing welcome the innovation but raise concerns about long-term affordability, especially for vulnerable populations such as seniors and the formerly homeless. LIHTC typically covers 30–40% of costs, leaving a gap that nonprofits fill with scarce public funds. For-profits like oWOW argue they can bypass this “gap financing” by reducing costs and attracting private capital.

Critics worry that for-profit developers may exit after the 10-year tax credit period, undermining affordability goals, and that developer fees may not support community services as nonprofit fees do. Still, many agree that lowering per-unit costs is essential to scaling housing production.

The debate highlights a broader industry shift: with construction stalled by scarce capital rather than zoning or permitting, both nonprofit and for-profit builders are rethinking how to finance and deliver housing. The outcome could reshape affordable housing in California, balancing innovation with equity and sustainability.

Learn more here.

Sleeping pods in San Francisco

Brownstone Shared Housing, the startup known for its $700-a-month “sleeping pods,” is planning a major expansion in San Francisco. The company has purchased a large building at 1049 Market Street, where it aims to install up to 400 pods—ten times the size of its current Mint Plaza location. These pods, each about four feet tall and designed to fit a twin mattress, are stacked in shared spaces with communal kitchens and bathrooms. The new facility is expected to open by summer 2026, pending city permits, and rents are projected to stay below $1,000 per month even as the company scales up.

The demand for this unconventional housing model seems strong, with Brownstone reporting thousands of applicants, especially among tech workers and downtown office employees looking for affordable options. In a city where median rents for apartments are around $3,065 and for one-bedroom units $3,500, the pods provide a significantly cheaper alternative. However, the company faces challenges: its Mint Plaza site previously faced eviction threats and permitting issues. Brownstone’s leadership insists they have learned from those setbacks and are positioning the Market Street project as a more stable, long-term solution to San Francisco’s housing affordability.

Learn more here.

Brownstone Shared Housing’s $700-a-month sleeping pods at 12 Mint Plaza in San Francisco (Source: Brownstone Shared Housing)

Master-planned communities

Maybe America needs some new cities like Irvine, CA

Conor Dougherty’s article in The New York Times (February 12, 2026) argues that Irvine demonstrates how the United States could meaningfully expand its housing supply only by embracing large‑scale, master‑planned development. He presents Irvine not as a typical suburb but as a purpose‑built city, shaped by unified land ownership, long‑range planning, and a willingness and ability to build entire districts at once. This, he contends, allowed Irvine to add housing, jobs, and infrastructure at a scale and speed that piecemeal zoning reforms in existing cities cannot match.

Dougherty emphasizes that Irvine’s economic and physical coherence—its research university, job centers, manufacturing base, and carefully designed residential “villages”—is the product of a deliberate, decades‑long planning philosophy. He notes that this approach is unusual in the U.S., where fragmented land ownership and local politics often prevent coordinated development. Irvine’s success, he argues, shows that building new cities from scratch is not only possible but may be necessary if the country hopes to address its housing shortage.

To explain how Irvine came to be, Dougherty cites Transforming the Irvine Ranch: Joan Irvine, William Pereira, Ray Watson and the Big Plan by C. Michael Stockstill and your curator. He uses the book to illustrate how the Irvine Ranch shifted from agriculture to a unified, master‑planned urban project. The book’s account of Joan Irvine Smith’s role in preserving the ranch as a single entity, William Pereira’s visionary plan, and Ray Watson’s disciplined implementation provides the historical backbone for Dougherty’s argument: Irvine’s success was not accidental but the result of intentional, large‑scale planning that is rare in American urban development.

Dougherty concludes that if the U.S. wants to build enough housing to meet demand, it may need to revive the idea of new, comprehensively planned cities, rather than relying solely on incremental reforms within existing ones. Irvine serves as the clearest modern example of what such an effort can achieve—and of how far current practice has drifted from that model.

What separates leading planned communities

In a post on LinkedIn, Gregg Logan of RCLCO, leading master‑planned communities succeed because they combine long‑term structural advantages with disciplined execution. Large-scale MPCs build resilience through economic cycles by leveraging brand strength, diversified housing, strong builder partnerships, and sustained investments in placemaking. Their performance is also shaped by geography: over the past decade, the Sunbelt—especially Florida, Texas, Houston, Central Florida, Las Vegas, and Phoenix—has dominated sales thanks to population growth, job creation, business‑friendly environments, and steady in‑migration. A small group of communities, including The Villages, Lakewood Ranch, and Summerlin, illustrate how long-duration platforms, consistent reinvestment, and clear identity translate into durable, repeatable success.

The most successful MPCs also excel at product segmentation. They offer a wide range of lot sizes, attached and detached homes, townhomes, and increasingly single‑family rentals, often supported by mixed‑use village centers and employment nodes. This internal ladder of housing options broadens the buyer pool and allows residents to stay within the community as their needs change, supporting absorption even when affordability tightens. Above all, lifestyle is the differentiator: top MPCs deliver extensive open space, trail networks, town centers, schools, healthcare, recreation, and social programming that make the community itself the primary value proposition. Buyers choose the place first, then the home.

Across decades of RCLCO’s survey data, the pattern is consistent: scale and brand matter, product diversity drives volume, Sunbelt growth remains powerful, lifestyle amenities shape demand, and well‑structured MPCs outperform through cycles. The best communities are not static—they improve over time through reinvestment, thoughtful planning, and a cohesive vision that integrates housing, amenities, and daily convenience into a compelling, enduring environment.

See Gregg Logan’s post on LinkedIn here.

Retail

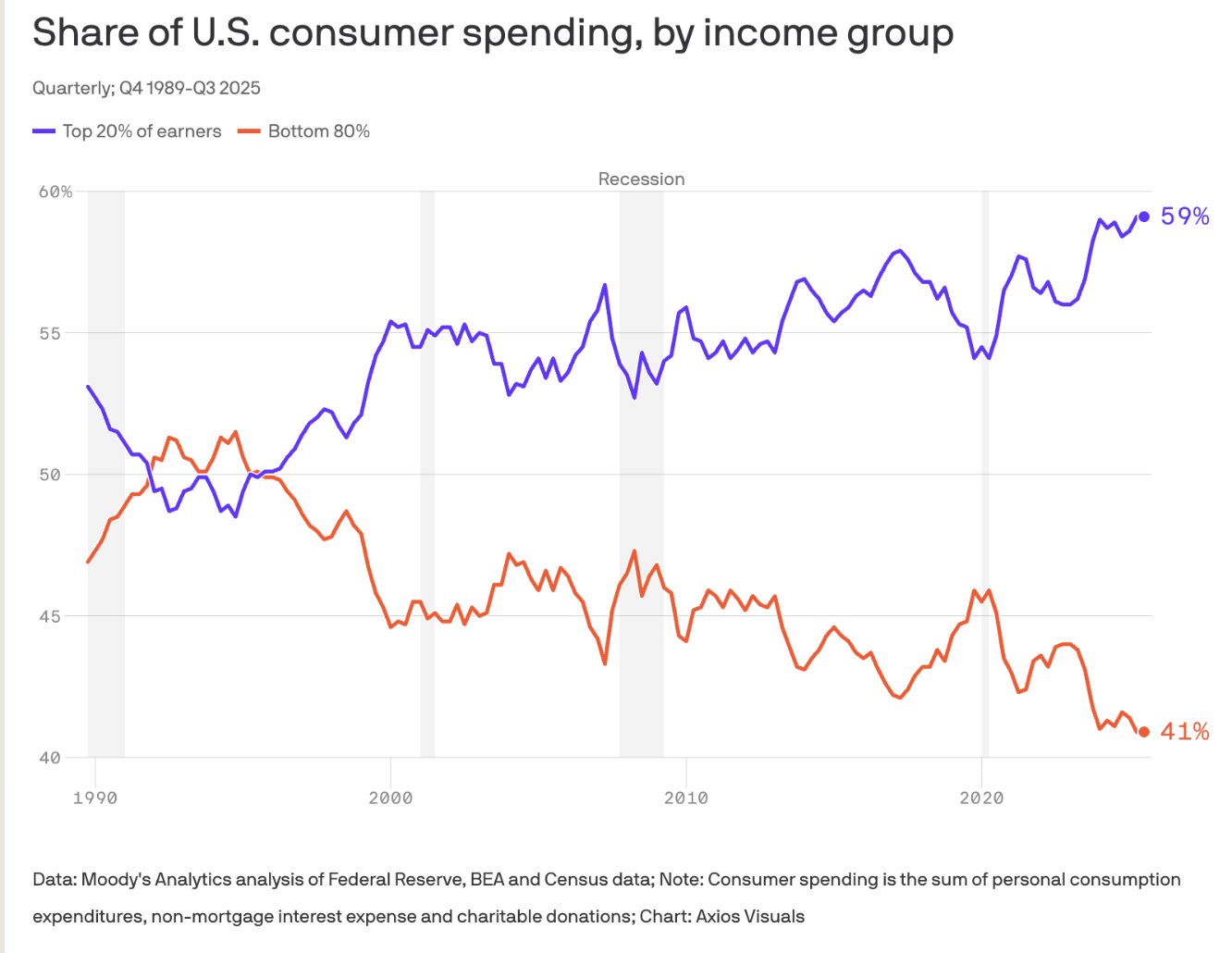

Top-heavy consumer spending in the USA

U.S. consumer spending has become steadily more concentrated among higher‑income households since 1970. In the early 1970s, the top 20 percent of households accounted for only the mid‑40‑percent range of total spending, meaning broad middle‑class participation still powered aggregate demand. By 1980, the top quintile’s share had risen to just under half, marking the beginning of a structural divergence tied to widening income inequality.

The decisive shift occurred by 1990, when the top 20 percent crossed the 50‑percent threshold and became responsible for half of all consumer expenditures. From that point onward, the concentration of spending at the top became a persistent feature of the U.S. economy. Through the 2000s and 2010s, Consumer Expenditure Survey data show the top quintile consistently at or slightly above half of all spending, while the middle 60 percent continued to lose relative weight.

Recent estimates highlight an even sharper imbalance. CES data for 2025 report the top 20 percent at roughly 35 percent of spending, but this is widely viewed as an undercount because affluent households are underrepresented in the survey. Moody’s Analytics, using Federal Reserve Survey of Consumer Finances data, estimates that the top 10 percent alone accounted for 49 percent of all spending in 2025. This implies that the top quintile almost certainly exceeds 50 percent.

The result is a markedly top‑heavy consumer economy in which aggregate demand depends increasingly on a small, affluent segment whose spending is less sensitive to economic shocks. Meanwhile, middle‑ and lower‑income households have diminished capacity to drive broad‑based growth, reflecting a long‑running erosion of their economic position.

Learn more here.

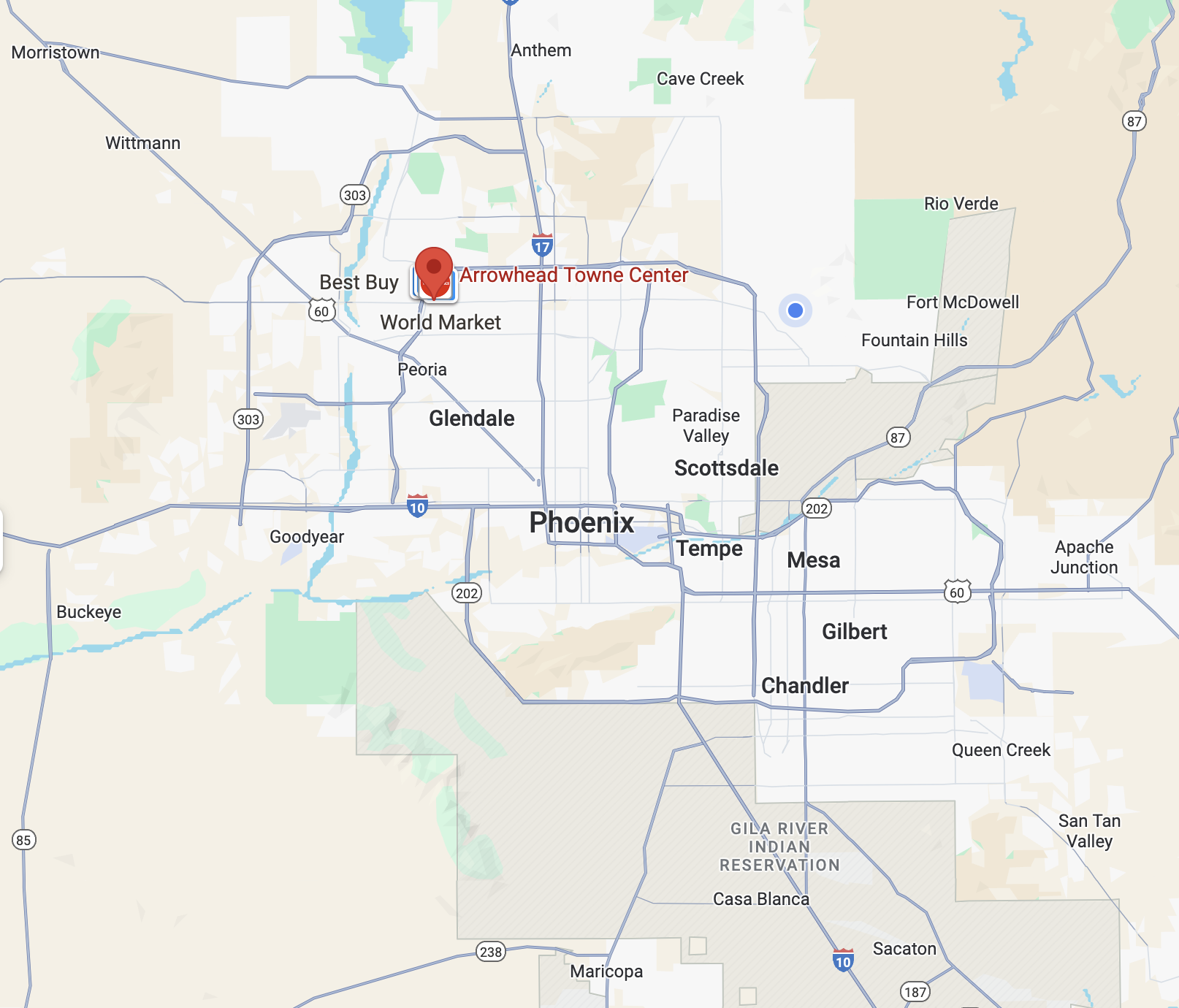

A mall that defines trends

Retail malls across the USA that were developed from the 1960s into the 1990s are being renovated, reworked, or reimagined. Then, there's Arrowhead Towne Center in the Greater Phoenix metropolitan area.

Unlike many of the now-defunct shopping centers in the region – Fiesta, Paradise Valley, and Metrocenter – Arrowhead in Glendale still resembles the mall that opened in the early ‘90s and is seeing more demand from tenants and consumers.

Arrowhead's owner, Macerich Co. (NYSE: MAC), doesn’t need to bring in high-end restaurants or seafood markets like its other mall properties in the Valley. As the only large-scale indoor shopping mall in Phoenix's Northwest Valley, it succeeds simply by being a traditional mall. It is home to the only Apple store west of Scottsdale, as well as several other major retailers.

Not only are there more people moving to the West Valley, but the ZIP codes in Arrowhead’s trade center have also seen an increase in higher-income residents, bringing more discretionary spending to the area, which has been a boon for Arrowhead.

Learn more here.

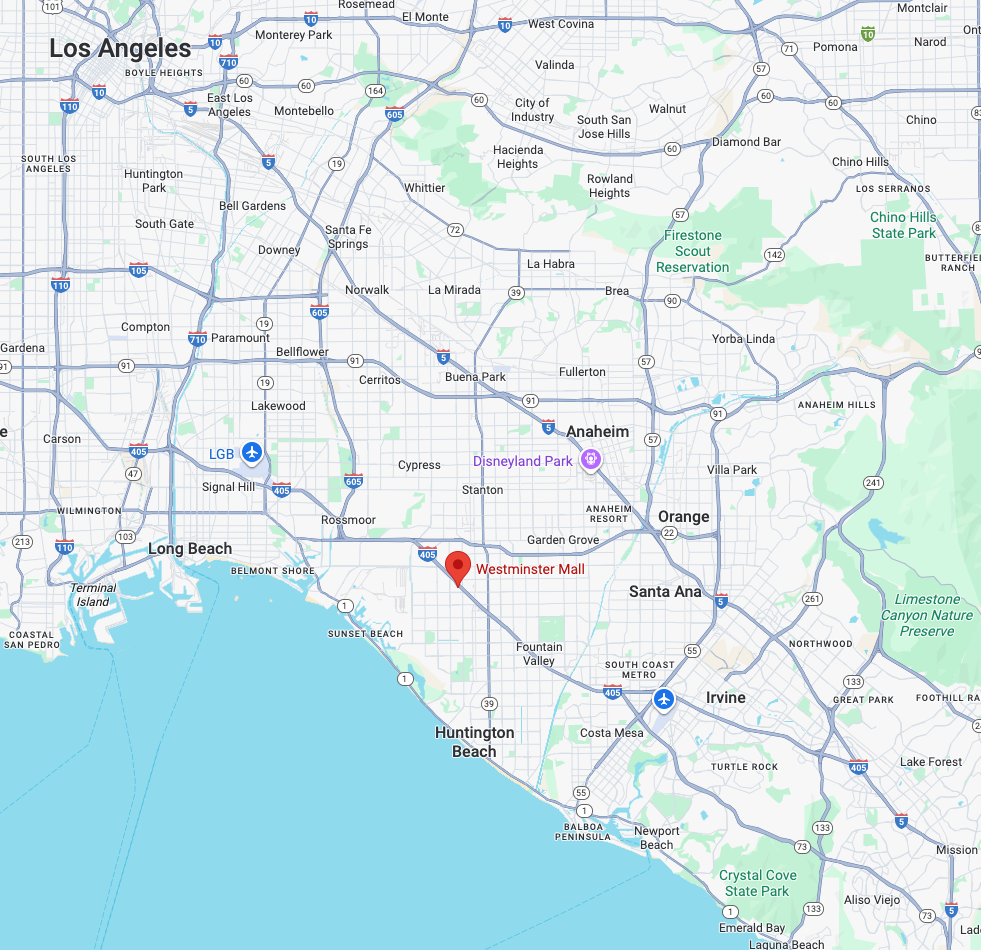

A mall that succumbed to trends

Located right off Interstate 405 just below the Los Angeles County border, the mall’s few remaining storefronts have been steadily shuttering over the last few months, with one of its final anchor stores — JCPenney — closing forever in late November 2025. A Target is the sole surviving tenant of this dying mall, with a bank, a Best Buy and an Outback Steakhouse holding down other corners of the vast parking lot. Now, most entrances to the mall are locked and boarded up, with only the occasional roller skater and biker doing donuts in the mostly deserted parking lot.

The roughly 100-acre property sits in a state of flux. Four separate corporate entities currently own pieces of the complex: The health care insurance giant Kaiser Permanente and the three retail firms Washington Prime Group, True Life Cos. and Shopoff Realty Investments. True Life has already been approved to build a five-story residential building on its portion of the site, part of a City Council-approved plan in 2022 that “envisions a lively, pedestrian-oriented environment featuring a mix of retail, restaurants, offices, medical facilities, hotels, and up to 3,000 new homes.”

A demolition date has yet to be set for the mall, and, given the fragmented ownership of the site, how it will shape up exactly remains an open question.

Source: Google Maps

The end of Sears

In late 2025, only five Sears stores remained open, and the long‑running unwinding of the Sears retail empire had reached another decisive chapter. An extensive New York Times article by Lauren Coleman-Lochner posted on December 26, 2025, reported on how Edward Lampert, the hedge‑fund investor who controlled Sears through its long decline, continued to shape the fate of Seritage Growth Properties, the real‑estate spin‑off created in 2015 to monetize Sears’ vast portfolio of stores and land.

The piece described how Seritage—originally pitched as a redevelopment engine that would turn old Sears boxes into mixed‑use assets—had instead spent years selling properties to pay down debt and satisfy investors. Lampert’s influence, both as Sears’ former CEO and as a major Seritage shareholder, remained a central theme: critics argued that the structure he engineered enriched financial stakeholders while accelerating Sears’ collapse. At the same time, supporters claimed the real estate strategy was the only rational response to retail disruption.

By 2025, Seritage was nearing the end of its liquidation plan, with most properties sold and the trust preparing to wind down. The article described this as the closing act of a two‑decade saga in which Sears’ retail decline, Lampert’s financial engineering, and the real‑estate monetization strategy became inseparable and ultimately failed.

Office

Remote work in the USA

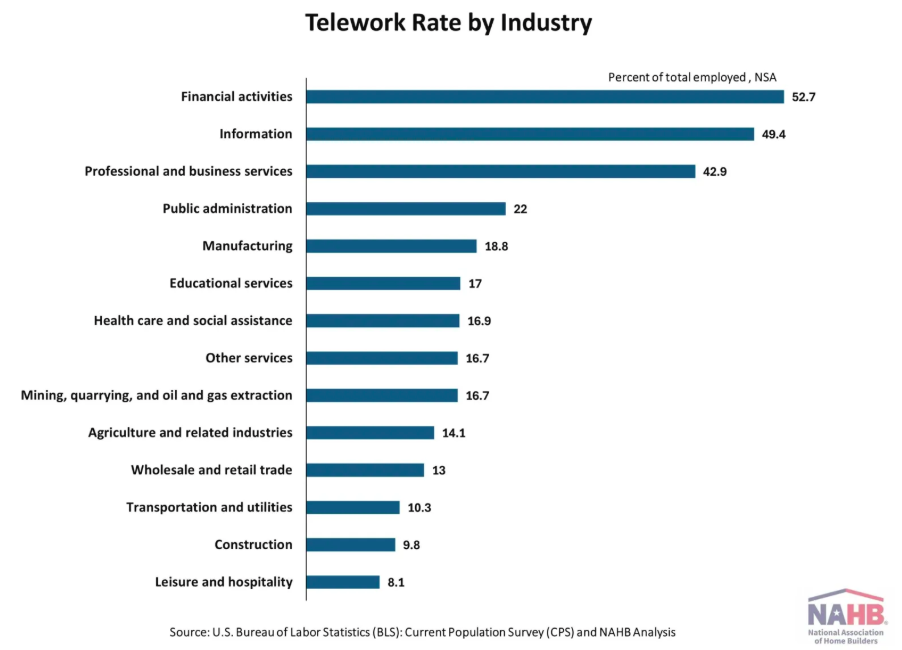

Remote work no longer defines the U.S. labor market as it did in 2020, but it remains a significant and stable feature of employment in 2025. Data from the Current Population Survey show that 34.3 million people—about 21.6% of all workers—teleworked in April 2025, a rate that has held within a narrow band since late 2022. More than half of these workers performed all their hours from home, while the rest worked remotely part time.

Telework participation continues to mirror longstanding structural divides. Women are more likely than men to work from home, with nearly one in four employed women teleworking compared with about one in five men. This reflects women’s concentration in professional and administrative occupations, as well as rising levels of college completion that position them in roles well-suited to remote work.

Age also shapes access to telework. Only 6.2% of workers ages 16–24 worked from home in April, compared with roughly 24% of those ages 25–54 and 23% of those 55 and older. Younger workers remain clustered in retail, hospitality, and service jobs that require physical presence, while older workers are more likely to hold managerial or specialized positions compatible with remote arrangements.

Education is one of the strongest predictors of telework. Just 3.1% of workers without a high school diploma teleworked, versus 38.3% of those with a bachelor’s degree or higher. Occupations and industries follow similar patterns: professional, technical, financial, and information-sector jobs dominate remote work, while construction, manufacturing, transportation, and leisure and hospitality remain overwhelmingly in-person.

Looking ahead, remote work appears durable but uneven. It continues to benefit workers with higher education and white‑collar roles, while those in manual or service sectors remain tied to on‑site employment. Whether telework broadens or deepens these divides remains uncertain.

Make it stand out

Whatever it is, the way you tell your story online can make all the difference.

Sources:

“U.S. women are outpacing men in college completion, including in every major racial and ethnic group”, Pew Research Center. https://www.pewresearch.org/short-reads/2024/11/18/us-women-are-outpacing-men-in-college-completion-including-in-every-major-racial-and-ethnic-group/

Connor Borkowski and Rifat Kaynas, “Telework trends,” Beyond the Numbers: Employment & Unemployment, vol. 14, no. 2 (U.S. Bureau of Labor Statistics, March 2025), https://www.bls.gov/opub/btn/volume-14/telework-trends-in-2024.htm

Suburban S.F. Bay Area office building to become apartments

Tourbineau Real Estate Partners, a Seattle-based developer, recently acquired the 3.4‑acre Tower Plaza complex in San Mateo for $22 million, a steep discount compared to its $77.3 million sale in 2019. The purchase followed foreclosure by TPG Real Estate Trust after the prior owner defaulted on a $75.8 million loan. Tourbineau’s plan focuses on converting the 12‑story tower into housing while keeping the four low‑rise office buildings in use. The proposal calls for 156 apartments averaging about 553 square feet, with a mix of studios, one‑bedrooms, and two‑bedrooms. Roughly 15 percent of the units will be income‑restricted, and residents will have access to amenities such as a lounge, gym, and landscaped courtyards.

The conversion will be overseen by TCA Architects, who intend to modernize the building with a refreshed facade, energy‑efficient windows, and new paint to highlight its concrete design. Tourbineau is leveraging California’s Density Bonus law, AB 2011, and SB 330 to streamline approvals and increase residential density. Located near Hillsdale Mall and within walking distance of the Caltrain station, the project is positioned as a transit‑oriented housing solution. More broadly, it reflects a growing Bay Area trend of repurposing vacant office space into housing, a response to high office vacancies in the post‑pandemic market.

Learn more here.

Tourbineau is working with TCA Architects on the conversion, which would create a mix of studios, one-bedrooms and two-bedrooms (Source: TCA Architects.)

Planning and zoning

Building in San Francisco Bay?

Facing $110 billion in projected flood defenses and a mandate to build 440,000 homes by 2031, San Francisco planners are reexamining land reclamation. A pilot concept at Hunters Point envisions 700 acres of new, elevated land hosting up to 20,000 homes—built for resilience and connected to transit infrastructure.

Unlike past reclamation models, this approach emphasizes green infrastructure, ecological sensitivity, and job-housing balance. Strategic shoreline expansion could reduce flood risk while opening space for mid-rise, affordable housing. A dozen such zones could fulfill most Bay Area housing goals and strengthen coastal defenses.

As climate and housing pressures converge, the Bay Area must choose between incremental retreat and transformative adaptation. Land reclamation could shift the paradigm—if regional governance aligns. With the right framework, the Bay could become a global model for resilient, inclusive urban growth.

Learn more here.

Concept plan for land reclamation at Hunter's Point in San Francisco (Source: Planetizen)

100 years of legalized zoning in the USA

Village of Euclid v. Ambler Realty Co. — a 1926 Supreme Court decision shaped the physical and social landscape of the United States more profoundly than almost any other ruling of the 20th century. By upholding a suburb’s right to separate land uses and exclude industry from residential areas, the Court effectively legitimized modern zoning.

Zoning’s core logic — segregating uses and restricting density — has produced the defining features of American development: suburban sprawl, automobile dependence, and the dominance of single‑family homes. It also constrained the supply of multifamily housing, contributing to today’s affordability crisis.

What began as an effort to impose order on chaotic industrial‑era cities — where factories, tenements, and immigrant neighborhoods were tightly interwoven — hardened into a regulatory framework that made mixed‑use, walkable neighborhoods illegal in much of the country.

On the 100th anniversary of the Euclid decision, zoning faces an unusual and powerful coalition of critics who argue that most zoning ordinances are outdated and harmful. They blame local land‑use rules for blocking apartments, worsening racial disparities in homeownership, and slowing infrastructure and housing production.

Reform is underway. According to the Mercatus Center, 33 states have enacted laws allowing more density in areas once reserved exclusively for single‑family homes. Thousands of communities have also re‑legalized mixed‑use development. These changes reflect a growing consensus that the century‑old zoning template no longer fits contemporary needs.

Learn more here.

Finance

Private credit has overtaken the banks

At his Construction & Capital Substack, John Friedrich explains how private credit quietly replaced traditional banks as the backbone of commercial real-estate finance. What began as a stopgap during the pandemic has become a structural shift in how projects get capitalized. The change didn’t happen overnight; it grew out of a decade of policy decisions and a new kind of lender appetite that prizes yield and speed over regulation and relationship banking.

From 2008 through 2021, the United States effectively ran on quantitative easing. The Federal Reserve bought trillions in mortgage-backed securities and Treasuries, holding rates artificially low and creating an ocean of cheap liquidity. Underwriting softened because lenders knew they could sell their paper into a hungry secondary market.

That era ended in 2022. The Fed moved to quantitative tightening, allowing roughly $30 billion of assets per month to mature off its balance sheet without replacement. Liquidity began to drain, spreads widened, and the same lenders who once courted every borrower started scrutinizing every deal. Projects that penciled at 3.5% debt suddenly faced double the interest cost.

As banks pulled back, private credit filled the gap. Pension funds, asset managers, family offices, and high-net-worth investors discovered they could originate debt directly and earn double-digit yields with asset-backed security. By 2023, non-bank lenders had surpassed traditional banks in total originations across many segments of commercial real estate.

Private credit behaves differently. It doesn’t rely on deposits, doesn’t sell paper to the Fed, and often has more flexible mandates. For developers, that means more creativity—non-recourse structures, interest-only terms, higher leverage—but also higher pricing and tighter covenants.

Two metrics define this new world: Loan-to-Cost (LTC) and Debt Yield. Debt Yield is simply net operating income divided by loan amount, and it has largely replaced the debt service coverage ratio (DSCR) as the sizing constraint. According to Friedrich, most lenders now target 6–8% at stabilization. If the yield clears, the deal can work, even without heavy recourse. If it doesn’t, no balance-sheet strength will save it.

Learn more here.

Fundraising for messy middle real estate investment managers

In one of his many Substack posts, Brandon Sedloff writes about how middle-market alts managers (alternative investment managers) have been too big to be specialists but not large enough to be a mega manager. He described them as being stuck in the “messy middle.” In 2025, private real estate funding rebounded, up almost 30 percent from 2024. Two firms—Blackstone and Brookfield accounted for 16 percent of that increase.

Now, as Sedloff talks to leaders of firms in that messy middle, he has come to realize that these firms often have deep sectoral or geographic specialization and a proven ability to scale. The challenging market conditions during and following the COVID pandemic required these firms to reimagine their business. Sedloff sees them as now prepared for a world where their size, scale, and history will be an advantage, not a challenge.

Learn more here.